About Farfetch

FTCH is accelerating the digitization of luxury industry. Broadly speaking Farfetch can be categorized into online marketplace and platform business.

Its online marketplace aggregates 3500+ luxury brands amongst which Farfetch owned NGG brand itself accounts to highest GMV than any other single brand.

The Platform business is much more interesting where it provides API integration and backend technology to power large luxury brands white label solution, which enables brands to scale and reach out to their direct consumers across the globe. In other words can we call it Shopify of luxury? Absolutely!

E-commerce marketplace as a model is not alone an exciting/sustainable model and it calls for having some sort of a value proposition. There needs to be a moat that company can control whether it is by controlling the Supply side or the having a robust tech enabled platform etc. otherwise which it’s easy for the competition to take over and eat away into your revenue.

Moats and value proposition

The future of fashion is no more about experiences in store but it is about getting those experiences online from the comforts of home. Gen Z is rapidly adapting to shopping luxury online and pandemic has pushed it even further at much faster rate. Farfetch and overall online fashion world will benefit from this trend.

Farfetch has smartly built multiple moats. It controls the supply side i.e. they have deals with plethora of small boutique stores from remote places of Europe and provides these businesses much needed consumer base across the globe.

The large brands and boutique stores alike would like to partner with a robust tech platform enabler instead of placing their efforts building their own omnichannel presence. Farfetch is trying to solve a painful problem for these brands i.e. connecting them to the affluent consumers in faraway places such as US, Middle East, China etc. They handle end to end e-commerce solutions i.e. everything marketing to inventory management to order fulfillment to customer service and returns.

Execution is pretty impressive:

• Acquisition of NGG brand in 2019 – This attracted a plenty of traffic as expected to the Farfetch online marketplace.

• Integration with Tencent’s wechat to make inroads into China.

• Tying-up with JD earlier and then pivoting to a much larger partner Alibaba which has 750M online users.

Visionary Founder led Company:

Jose Neves is the founder and CEO – a visionary in online fashion industry with many years of toil behind him. He has built farfetch ground up since 2008.

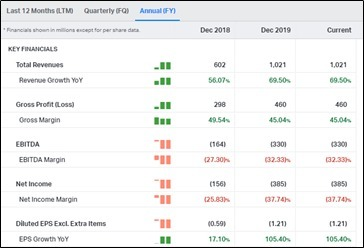

Take rate of Farfetch is at whopping 37% of GMV, which is mostly unheard of especially in e-commerce. To compare Shopify’s take rate is a mere 2.5%. This is not necessarily a good thing for Farfetch as any leverage to increase the existing take rate could be hard. Anyhow this big take rate number suggests that Farfetch is a very important partner for these brands and they are willing to pay up such high premiums to be on Farfetch marketplace or to use its platform.

Inroads to China and Invasion of China:

Luxury consumption starts with China and ends with China. In other words whoever captures China will be the king of online luxury. Currently China alone makes 36% of luxury market and it’s expected to grow to 50% by 2025. So in literal sense, it’s half the battle won if you win China.

Farfetch gives Chinese affluent, access to remote boutiques in Europe. On the other side it also opens the doors to the world of luxury fashion which is unique.

Alibaba and Richemont invested more than $1B to form joint venture with Farfetch China for a combined share of 25%. This allows Farfetch to integrate with Tmall (luxury online store) of alibaba giving it’s partners/brands access to 750M Chinese consumers.

Competitors – Not threatening Farfetch much:

Why Amazon cannot win this game

Luxury game is different, it’s all about branding, having exclusivity and presenting those elevated and inspiring experiences.

The brands are hesitant to work with Amazon as they worry more about counterfeit products and dilution of branding. Amazon is creating an exclusive app for luxury shielding it from the regular amazon app but

I can surely get an original Oscar de la renta for two grand on amazon luxury app but probably be able to get a close imitation too on Amazon regular app for hundred bucks. That’s the stigma that Amazon will have to fight.

Moreover Amazon is almost closing its shop in China after accepting the defeat to Alibaba and JD. 50% of luxury market is already ruled out where Farfetch is making impressive strides striking deals with all the mega empires of China such as Alibaba, JD and Tencent.

Yoox Net A Porter (YNP) – Once a competitor turned into a partner

YNP is owned by Richemont group and is a big player in luxury digital marketplace business. However they are losing money by the day. Their model is to buy the inventory from the brands and sell it on the platform apart from powering the backend of some brands just like farfetch. However being inventory heavy is not a compelling business in the modern day and is generating losses for them. In contrast Farfecth operates in an asset light fashion.

Interesting thing is once a competitor YNP invested in Farfetch China business along with Alibaba. Farfetch is more platform heavy and less a brand by itself. YNP has brand interests and it wants to promote Richemont brands and gain stronghold against competitors like LVMH and Kering in China and elsewhere. So Farfetch really is a partner to the big luxury groups and not a direct competitor which really positions Farfetch far from competition.

Risks:

37% GMV take rate could be a risk, as they may not have additional room to increase the rate. Easy for competition to offer lower take rates. However this risk is not a problem in the near future as Farfetch has contracts in place with the 1000s of brands which want to be on its platform despite this take rate.

China is a matured ecommerce where users easily adopt to buying online. However it is to be seen how rest of the world’s affluent will behave after the pandemic, do they want to visit fashion stored in Europe themselves and shop in person to gain those experiences? This is a risk to the online market but the future projections show the new gen wont mind splurging on shopping online and think it is cool to participate in auctioning bragging about the experiences on the social media.

Conclusion:

E-commerce is a growing trend to sail on for next decade as more and more users adopt to it. Luxury online shopping is no different. Pandemic mutli-X’d online shopping adoption and behavior. Experts think much of that behavior is going to stick. Farfetch is growing at a fast clip especially in China market which is going to make up 50% of overall global luxury market by 2025. Even the competitors like Yoox-Net a porter (Richemont group) investing in Farfetch makes me much more bullish. I feel like I am sitting on a multi bagger which will unfold itself in next 5 years to come.