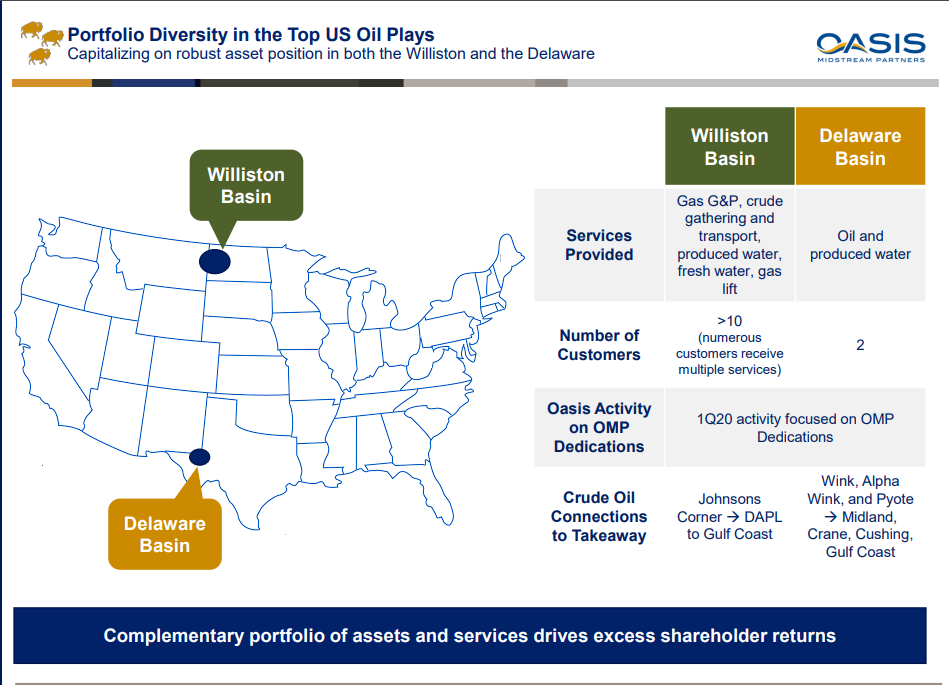

- Oasis Midstream Partners is a 3-year-old MLP, that operates in Williston Basin & Delaware Basin

- Oil and Gas volatility due to Covid 19 has created a lot of uncertainty for E&P and MLPs.

- OMP (Oasis Midstream Partners) has cash coverage of 1.6x-2.1x and growing

- Gas and Oil price volatility due to OPEC can create havoc for MLPs

What are MLPs?

MLPs are Master Limited Partnership that are limited partnership.

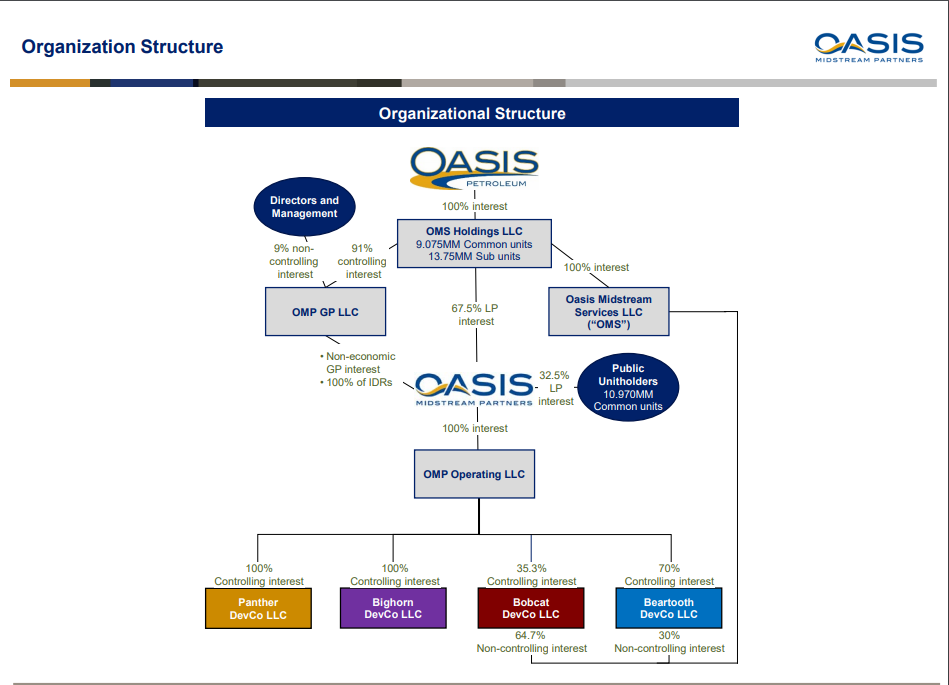

MLPs take advantage of cash flow, as they are required to distribute all available cash to investors. OMP is one such MLP that was spun off from OAS (Oasis Petroleum Inc.) back in September 2017, OAS is an E&P (Energy and exploration company)

Best way to Describe an OMP business model is a toll road, they own processing/transporting pipelines and Water gathering and disposal. Fresh water distribution, storage tank and natural gas processing facilities in Delaware and Williston Basic.

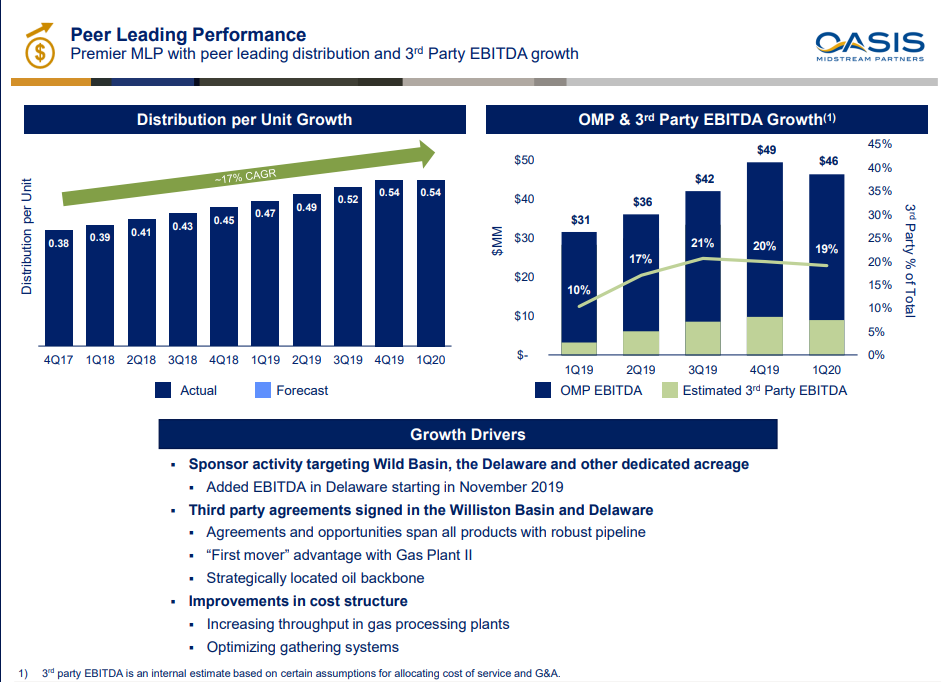

OMP has been able to grow Distribution per unit at 17% CAGR and have been diversifying 3rd party volume from OAS.

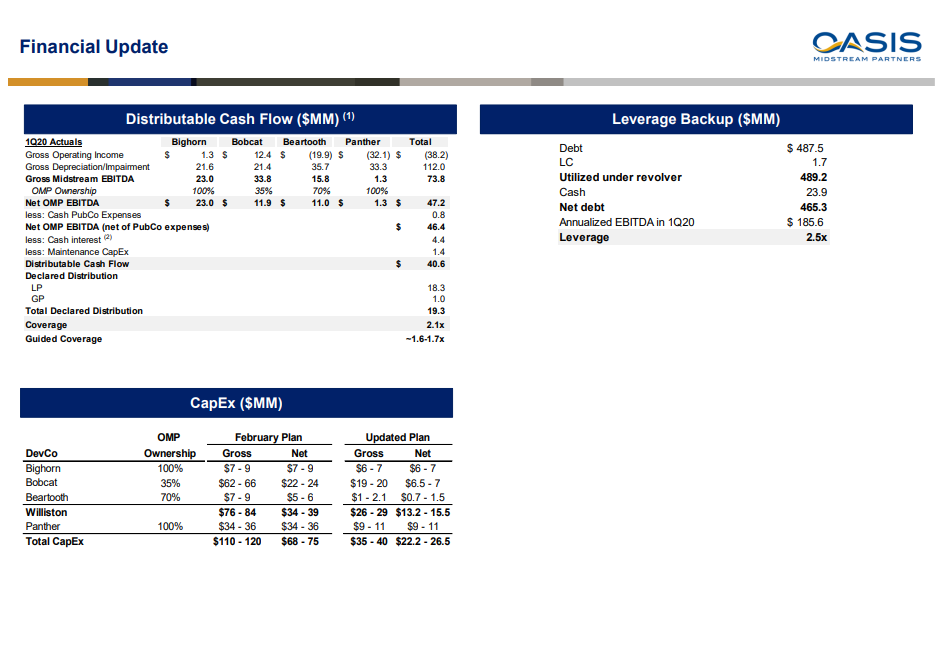

Our focus is whether OMP can sustain paying dividend at current level comfortably and continue to grow it as needed. for Q1 2020 OMP has Net Distributable Cash flow of $40.6 million and Total Dividend of only $19.3 million giving it a coverage ratio of 2.1x.

OMP leverage ratio is 2.5x which is very low relative to the industry and should allow them to grow comfortably. They also are reducing CapEX for 2020 by 45.8-48.5 million that should free up additional cash for dividends.

Currently OMP is offering $2.16 dividend or 0.54 cents Quarterly almost 22% annualized, for 2020 I do not predict OMP raising dividend but maintaining current levels.

Risk:

The volatility risk from the underlying price of Oil and NG (natural Gas), Saudi and russia are currently maintaining OPEC production cut however they may decided to increase that to protect their market share.

Additional production from fracking and continued weakness in Economy and world market demand due to COVID.

OAS parent company which has a higher debt load and is an E&P currently owns 67.5% of the OMP MLP may force a merger or a reverse buyout.

52 week Low 2.80

current price : 9.60

Investing in OMP is a long term accumulation, under $8-10 range is prudent.

Price above $12-14 does create adverse risk for pull back, on a normalized market Yield should stablize at 14-16% if current payout is maintained we can see Price Fair value at $16 dollar creating 60% upside over next 12 months.

Additional disclosure: Disclaimer: The information presented in this article is for informational purposes only and in no way should be construed as financial advice or recommendation to buy or sell any stock. The author is not a financial advisor. Please always do further research and do your own due diligence before making any investments. Every effort has been made to present the data/information accurately; however, the author does not claim 100% accuracy. The stock portfolios presented here are model portfolios for demonstration purposes.

Disclousre: I am currently long in OMP.