- Zen Desk (Zen) is a software-application company that provides solutions, sales, CRM, customer support SaaS

- Zen competes in a crowded market against a behemoth like Salesforce, Hubspot, SAP, Oracle, and Microsoft.

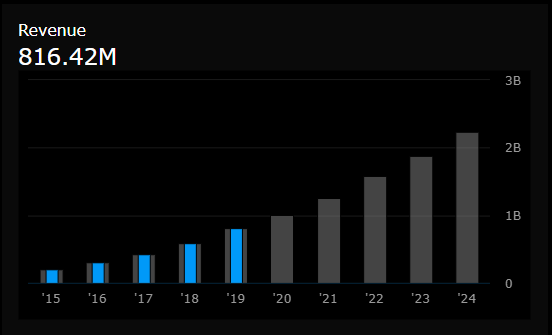

- Company has been growing Revenue at 31% y/oy and projected to grow at a high rate for the next 5 years

Zen Desk started as a support software for customer agents to be able to solve issues in 2007 and now it has morphed into one-stop solutions for clients. They have the following offerings of software.

Zen’s flagship product is the Support suite which allows customer service agent to open & resolve issues. Zen also has The Sales Suite, which is a CRM to enable companies to cross sell and manage product campaigns.

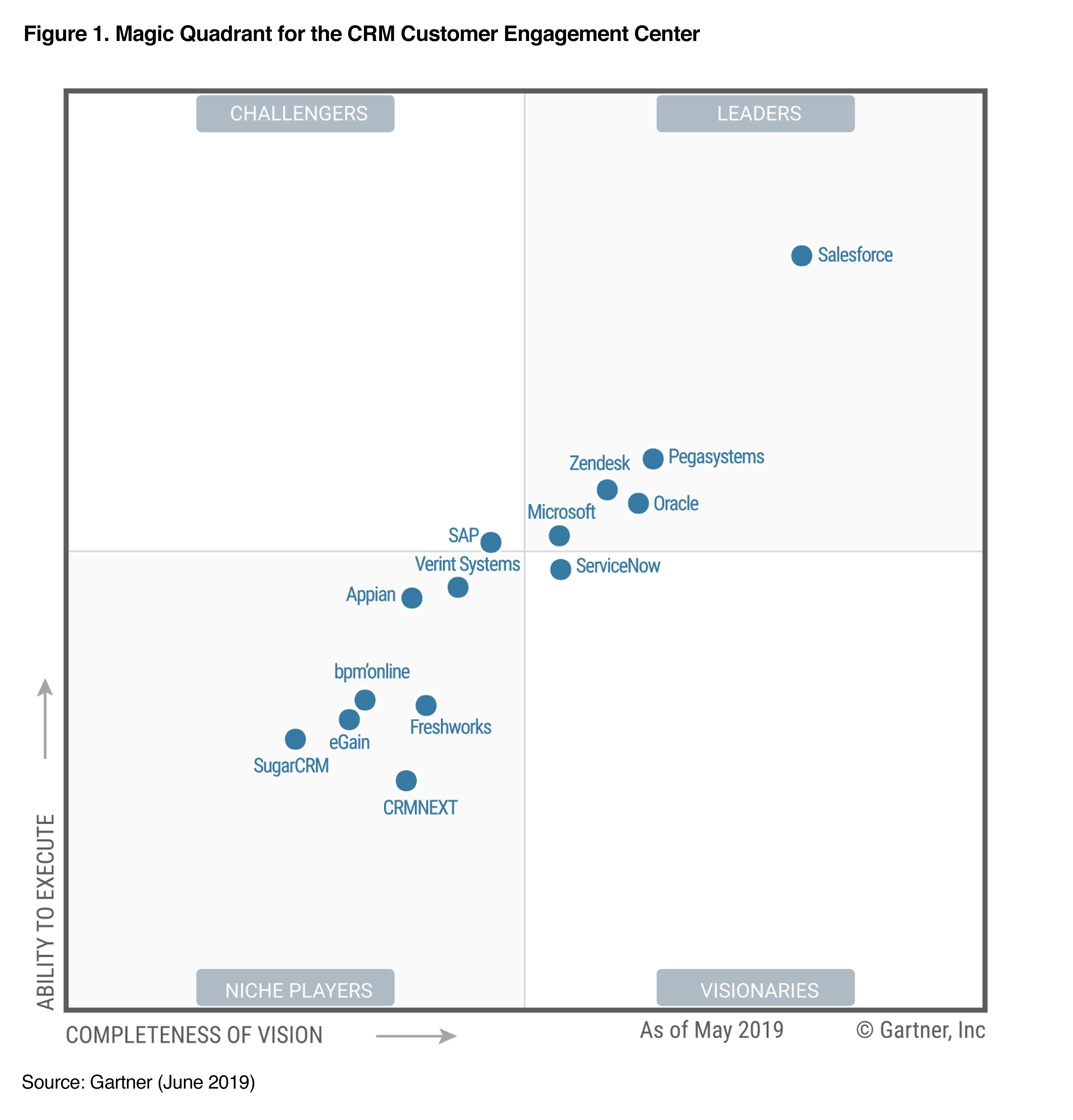

Zen competes with the likes of Salesforce, Oracle, Microsoft, ServiceNow, SAP, SugarCRM etc. However, they land on the right side of Gartner’s magic quadrant and have been moving in the correct direction in terms of software offering, and innovation.

Zen is projected to grow revenue 20%+ CAGR and current analyst estimate for 2024 Revenue average is 2.24 Billion.

Zen being a SaaS company has a high gross margin of 74% and has been expanding gross margin in recent quarters. The current debt is approx $597.8 million and cash on hand of $468.1M.

The current market cap is approx $9.7 Billion, and outstanding shares tend to grow approx by 2-3%.

52 Week Low of $50.23

Current price of $84.80

Conclusion:

Zen desk can be a Zen for your long term portfolio, It currently trades at $84.80 and has Resistance at $90-$94.89 range, Long term support of $60-$65 range. I am currently accumulating ZEN at 5-10 shares with long term goal of acquiring approx 100-150 shares.

My initial entry point in Zen was of 25 shares at $72 and I plan to be fully vested with 100-150 shares in the next 3-6 months accumulating 5-10 shares every few weeks depending on the price. I will not add shares above $90 and may even divest some if it runs above $120 in the short term. I plan on keeping Zen 2+ years or Target price of $125-175, as I believe in the long term viability of the company and its growth.

Risk:

Although net customers have been growing at a healthy rate, Paid customers using Zendesk Chat did decrease by 10% over 1 year.

Zen will need to continually innovate to keep up with deeper pocket players like Salesforce, Oracle, Microsoft, affecting Cash flow and EBITDA. Zen has a disconnect between Value and valuation and any re-alignment in valuation multiples can contract the share price. Loss of employment due to COVID can reduce the number of customer service agents affecting revenue short term.

Additional disclosure: Disclaimer: The information presented in this article is for informational purposes only and in no way should be construed as financial advice or recommendation to buy or sell any stock. The author is not a financial advisor. Please always do further research and do your own due diligence before making any investments. Every effort has been made to present the data/information accurately; however, the author does not claim 100% accuracy. The stock portfolios presented here are model portfolios for demonstration purposes.

Disclousre: I am currently long in ZEN.